Most CFOs treat lead time as an operations problem. I did too, until I started noticing what it was quietly doing to our working capital, our headcount, and our margin. It turns out flow efficiency isn't a process initiative at all. It's one of the most underused financial levers on the balance sheet.

I’ll be honest — when I first came across the term flow efficiency, I assumed it was an operational topic. Something for the COO to worry about. Not my department, so to speak.

Then I started looking at what lead time was actually doing to our numbers. It was hiding in the Profit and Loss the whole time. In the working capital we couldn’t explain. In the over-hiring we justified as “growth.” In the firefighting that somehow never stopped costing us money.

That is when it clicked.

The cost of silos isn’t visible - until it is

Most organizational charts look clean on paper. In reality, most functions behave like separate companies. They plan separately, staff separately, and optimize separately. Work piles up in the gaps between them. Nobody owns the wait time. And that wait time is quietly shrinking your margin.

The problem is that it rarely shows up neatly in a Profit and Loss. It hides in delayed revenue, bloated inventory, and the endless cost of fixing symptoms instead of causes. More headcounts here. Emergency outsourcing there. It feels like progress, but you’re just running faster down the same broken track.

What flow efficiency actually does to your financials

The principle of flow efficiency is simple: align your teams around end-to-end value streams, improve hand-overs and cut the wait times. Then watch what happens to the numbers.

And I don’t mean that abstractly. Here’s what it’s looked like in practice across some of companies that have implemented Hups’ strategies:

- A logistics operation cut deviations by 85% and lifted output by 30% in just five months

- A forestry business reduced lead time from 198 to 45 days, freeing up significant working capital in the process

- A global manufacturer brought parts supply lead time down from 12 to 7 days, reducing stockouts and expediting costs across the board

A 30% increase in output doesn’t just improve customer service, it translates into higher revenue on the same fixed-cost base. That is pure margin expansion.

A 79% reduction in lead time cuts work-in-progress inventory and frees up capital locked in operations. For a mid-to-large company, that can mean tens of millions released back into cash flow.

And reducing parts supply lead times from 12 to 7 days wasn’t just about speed. It meant fewer stockouts, lower expediting costs, and greater service stability. Those benefits flow straight to the bottom line, often outweighing the initial investment in training or systems.

These aren’t operational wins dressed up as financial ones. They are financial wins. Better cash flow. Lower Operational Expenditure. Stronger return on assets.

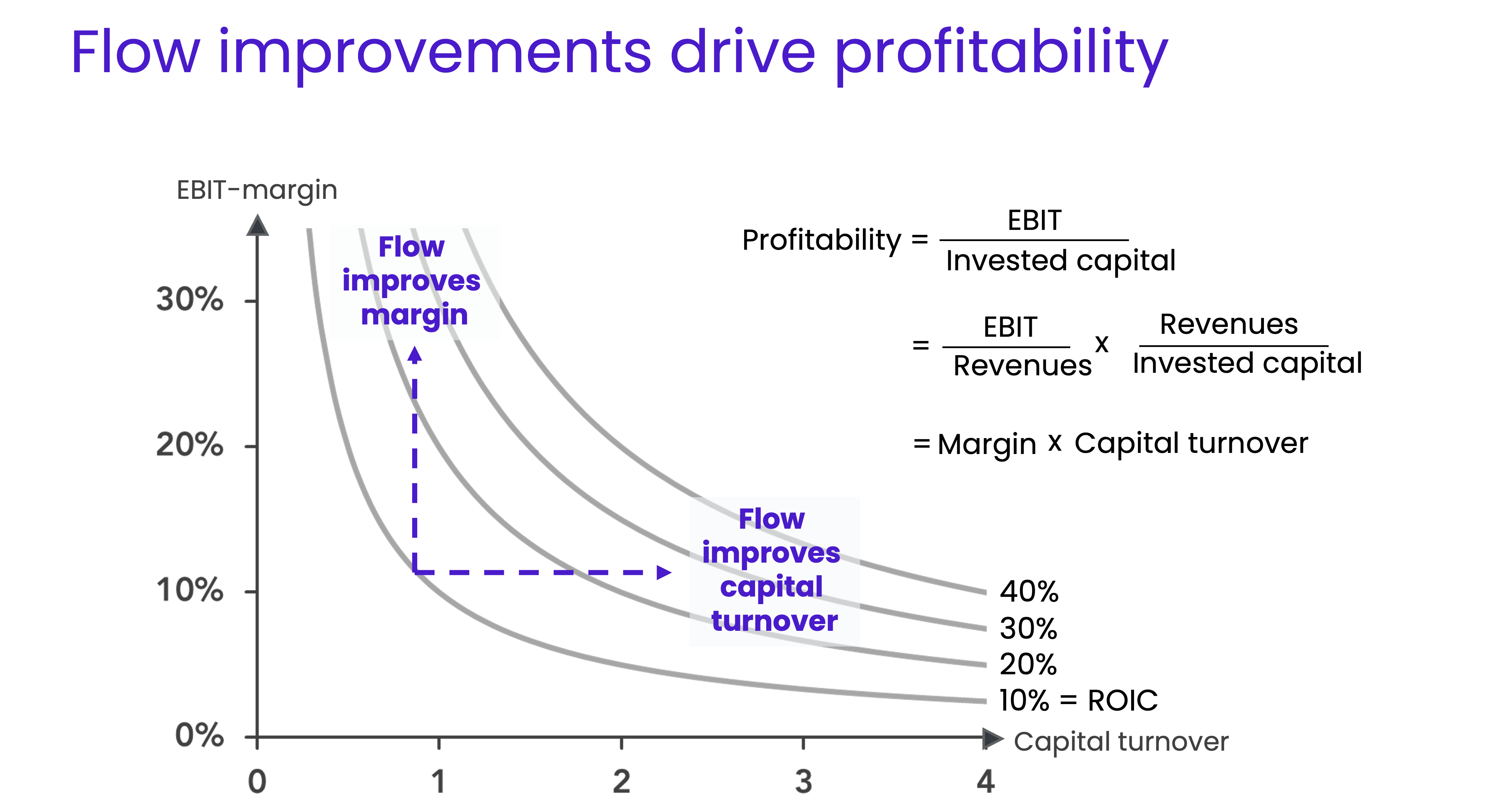

Why this hits both sides of the ROIC equation

As CFO’s, we think in return on invested capital. What’s interesting about flow is that it moves both sides of that equation at once.

Faster flow means faster delivery, which means faster revenue. At the same time, shorter lead times cut inventory, reduce rework, and eliminate the hidden labor cost of constant firefighting. Your costs go down while your output goes up.

But the balance sheet impact is where it really gets interesting. Shorter lead times mean less working capital tied up across operations. You’re not just improving your margin, you’re reducing the capital required to generate it. That’s a different kind of win, and it’s one that most cost-cutting exercises never touch.

Buying speed vs. building it

There’s a reflex most of us have when things get slow: hire more people, add more tools, outsource the bottleneck. It works, in the short run. Then it shows up as bloated Operational Expenditure and you’re back in the same conversation six months later.

Real, scalable speed isn’t bought. It’s built by removing the systemic friction that slows work down in the first place. Companies that do this well consistently free up 15 to 20% of operating costs - not by cutting people, but by cutting waste in the flow.

That’s a different conversation than headcount reduction. And to be honest, it’s a much easier one to have.

What I’d ask you to reconsider

If you’re a CFO and lead time lives on your operations dashboard but not in your financial thinking, that’s worth changing.

Lead time is a direct lever on cost, working capital, revenue timing, and risk. It belongs in the same conversation as margin and ROIC, not siloed off in the operational review that you half-attend.

Flow efficiency isn’t a process improvement initiative. It’s a financial strategy. And once you start seeing it that way, it is hard to unsee.

More on flow and financial performance -> Read about the Danish medical company that had numerous initatives going company wide, high activity level but yet results were missed out.